|

|

April 24, 2012 Hospital of Cards

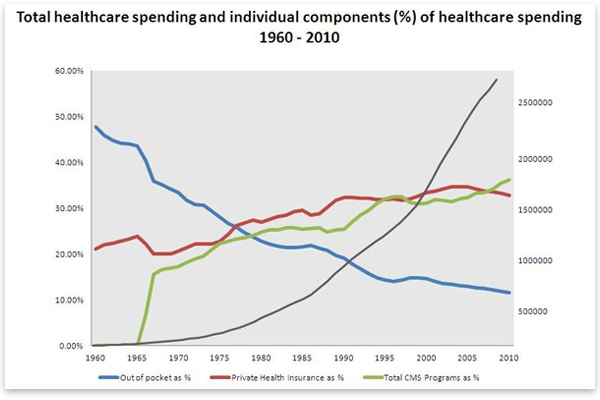

For some perspective on the magnitude of the healthcare bubble consider that from 1990 to 2007 the cost of all items, as measured by the Bureau of Labor Statistics (BLS), rose by 159 percent while housing rose 163 percent and medical care rose a staggering 216 percent. A recent study by the Kaiser Family Foundation found that between 1999 and 2011, health-insurance premiums increased 168 percent while workers' total earnings increased only 50 percent. As figure 1 demonstrates, healthcare spending increased dramatically when the government (represented by total CMS spending in green in the figure) began subsidizing healthcare for the poor and elderly through Medicare and Medicaid. It continued to increase as legislation, most notably the HMO Act of 1973, and regulatory policy shifted the responsibility of health maintenance from the individual to all of those in his or her insurance pool. This was accomplished through regulations requiring insurers to cover medical services (e.g., office visits, cancer screenings, pharmaceuticals, and a wide range of therapeutic and rehabilitative services) for conditions that were not insurable events but rather part of routine health maintenance. Throughout the expansion, out of pocket spending (represented by the blue line) declined dramatically.

America's healthcare system today can best be described as what economics professor Thomas DiLorenzo has termed "fascialist." According to DiLorenzo, "Fascialism means an economy is part fascist, part socialist." Fascism is characterized by private enterprise that is comprehensively regulated and regimented by the state, ostensibly "in the public interest" (as arbitrarily defined by the state). A variant of fascism is crony capitalism. Socialism started out meaning government ownership of the means of production, but it has come to mean egalitarianism promoted by progressive taxation and the institutions of the welfare state. According to DiLorenzo,

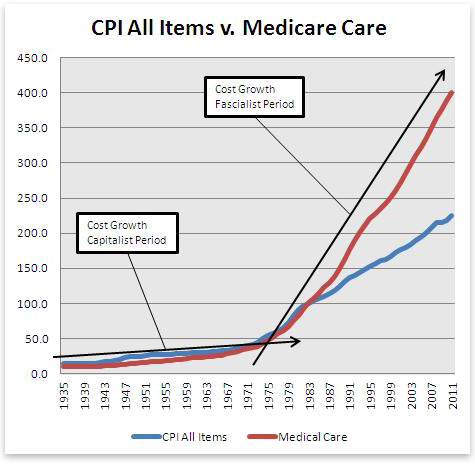

Under the current system, consumers play virtually no role in shaping the pattern of resource use and the assignment of resource rewards. The outputs being produced, the methods of production being employed, and the rewards being given to the various owners of productivity are not dictated by healthcare consumers but rather by government and industry lobbyists, or the medical-industrial complex. This mechanism is directly responsible for inflating the healthcare bubble and costs have grown rapidly to reflect whatever the system will bear. Prior to Medicare and Medicaid and the significant regulatory changes that have taken place, the healthcare system actually operated under near-capitalist conditions (it was never pure capitalism). I will term this the capitalist period of US healthcare. During this time, individuals paid for the majority of medical goods and services out of their own pockets and utilized health insurance as a rational tool for mitigating financial risk posed by catastrophic events. Although still a relatively new concept, participation in private insurance plans was growing, and by 1960 nearly 75 percent of Americans had some form of private health-insurance coverage.[1] During this period, rapid advancements were being made in pharmaceuticals, diagnostics, and surgical techniques (e.g., the heart-lung machine, which made coronary artery bypass surgery possible). Furthermore, charitable institutions and hospitals often run by religious groups and fraternal organizations such as the Freemasons, whose mission was to take care of the indigent, abounded. Most importantly, the price of medical goods and services remained remarkably stable as measured against the consumer price index (CPI) for all items:

As figure 2 demonstrates, medical-care price inflation corresponded with the change from the capitalist to fascialist model. The practice of medicine under the current system is less about providing patients with what they value and instead providing them with what is profitable to the medical-industrial complex. The game is rather simple; the outline follows:

This process may seem rather benign, if not beneficial — it may even seem like good capitalism — but it is not. Obscured by this process is the fact that what often passes for "statistically significant" would be viewed by many patients as "clinically irrelevant" and thus not worth near the amount that Medicare or their insurance carrier reimburses. I'm not suggesting that these products and services should not be allowed to come to market. I'm simply suggesting that, given their risk-reduction profiles, under free-market conditions many of them would need to cost much less to be attractive options. A great example is the drug Rivaroxaban. It has been approved for usage to lower the risk of stroke in patients with atrial fibrillation. However, a recently hyped clinical trial may expand its use significantly. The trial, reported on in the Janurary 5 issue of the New England Journal of Medicine, showed that Rivaroxaban, when combined with standard therapy, lowered the absolute risk of death, heart attack, or stroke by 1.9 percent over a two-year period in patients who had recently had a heart attack.[2] To be precise, those taking Rivaroxaban had an 8.9 percent risk while those not taking it had a 10.7 percent risk. Also of note, taking Rivaroxaban increased the risk of a major bleeding event by 1.5 percent (those taking it had a 2.1 percent risk, while those not taking it had a 0.6 percent risk). Given this information, how much would this drug be worth to you for the above indication, if at all? If your answer is not hundreds of dollars per month then you can appreciate why I believe healthcare is a bubble. The above example is not an exception but rather the rule. Just within my own field of cardiology there are numerous examples (e.g., whether or not to get a stress test and what kind of stress test to do, how often to do an echocardiogram for a patient with asymptomatic valvular heart disease, how often to check cholesterol levels in patients with and without known heart disease, whether to use a stent or thrombolysis to treat an acute heart attack and what type of stent to use, whether to use brand name or generic drugs for blood pressure and cholesterol lowering and when to start these agents in the first place). In my opinion, these few examples demonstrate how and why the healthcare bubble has grown so massive. In almost each case, the standard of care for the particular issue in question endorses more frequent use and the use of expensive agents and modalities over less frequent and less costly alternatives; however, the absolute benefits of the more frequent and expensive options are usually quite small (if they exist at all) as in the case of Rivaroxaban above. These examples demonstrate why government-subsidized healthcare has been a panacea for the medical-industrial complex. But unfortunately, what cannot go on forever must come to an end. Government healthcare spending has continued to accelerate rapidly over the last decade. The government now directly pays for over half of all healthcare costs in the United States. But more importantly (and this point cannot be overemphasized), Medicare approval drives reimbursement for nearly all medical goods and services whether paid for by the government or private insurers. At present, nearly half of Medicare is financed through general revenue (revenue not generated through dedicated payroll taxes and premiums charged to beneficiaries) and the federal government is running huge budget deficits that are not sustainable. There is simply no way the federal government can indefinitely prolong the trend in healthcare spending. According to John Embry, chief investment strategist for Sprott Asset Management,

There is no circumstance under which this degree of government spending can be financed indefinitely, and when it's not, the slack won't be taken up by individuals. Dr. Gilbert Berdine emphasized this in a 2011 article. Some of the salient points he highlighted include the following: In 2008, HHS estimated that national health expenditures per individual were $7,845 — over $31,000 for a family of four. At the same time, the Census Bureau claimed that the average household size was 2.63 and thus, the average household share of national health expenditure was $20,632. The census estimated that almost one-fifth of US households earn less income than their share of national health expenditure. Regardless of their desire to do so, US citizens as a whole cannot afford what the United States spends on healthcare, and therefore I believe that, when government spending on healthcare declines, the healthcare bubble will burst. This could be brought about in several ways, such as a failure to raise the debt ceiling, as Dr. Berdine has pointed out; a failure by the government to raise capital at historically low interest rates, as John Embry alluded to; or government policies that actually reduce healthcare spending, like not renewing the infamous "doc fix," using the Independent Payment Advisory Board (IPAB) to restrict which patients are eligible for certain medical care, or simply having CMS reduce reimbursement rates, which doesn't require any new laws or changes to existing law. ConclusionEntangled in the current debate over the constitutionality of the Patient Protection and Affordable Care Act (PPACA), there are very few who have given much thought to the idea that healthcare could be a bubble. At the moment, I'm engaged in a debate with a reviewer at a particular medical journal who flat out denies that a healthcare bubble is even plausible. According to this reviewer,

On this point, I challenged the reviewer that shelter is a basic need of life, yet the housing bubble collapsed. I got no response. This reviewer, who I assume is a physician, displays the same hubris as so many others in the medical field — the idea that all healthcare goods and services are indispensable and, ultimately, either save or have a tremendous impact on the quality of one's life. The fact is that very few healthcare goods and services immediately impact whether an individual lives or dies, and most of their benefits will go unnoticed by the individual patient. Instead, most of these goods and services, whether consumed in the inpatient or outpatient, setting lower the medium- or long-term risk of something or another by a few percentage points and, in the end, we still die anyway. The value of this risk reduction is ultimately subjective, but because of the policies mentioned in this paper, and the government's ability to support those policies by borrowing money at artificially low interest rates, many individuals have never had to give much thought to the value they would place on the medical goods and services they consume. Unfortunately, due to our deteriorating fiscal condition as a nation, the day will soon come when the government can no longer subsidize healthcare to the extent required to keep the bubble inflated. At that point, individual patients will have to choose whether or not to pick up the slack. When that day comes, look out! Andrew Foy is cardiology fellow at Penn State-Hershey University Medical Center. The opinions expressed here are his own and are not intended to represent those of his employer. Send him mail. See Andrew Foy, MD's article archives. Copyright © 2012 by the Ludwig von Mises Institute. Permission to reprint in whole or in part is hereby granted, provided full credit is given. Notes[1] Source Book of Health Insurance Data, 1960, Health Insurance Institute, 1961. [2] Mega, JL., Braunwald E., Wiviott SD., et al., "Rivaroxaban in Patients with a Recent Acute Coronary Syndrome," New England Journal of Medicine 2012; 366: pp. 9–19. Back To It Takes Brains

|

The US healthcare system is a huge bubble fueled by misguided policies that are sustained by the government's ability to borrow money at artificially low interest rates. When either the policies change or the flow of credit to the US government stops, the bubble will burst.

The US healthcare system is a huge bubble fueled by misguided policies that are sustained by the government's ability to borrow money at artificially low interest rates. When either the policies change or the flow of credit to the US government stops, the bubble will burst.